Selling Assets Versus Equity

One of the more critical initial items to consider when selling a business is determining whether the sale involves selling the equity or assets of the business. The choice of structure will have an impact on several items, including, (i) the tax consequences to each of the buyer and seller, (ii) the party responsible for the company’s liabilities, and (iii) third-party consents required to consummate the transaction. In many cases, the buyer and seller will benefit differently depending on the structure, so it is important for the seller of a business to fully understand the impact of each structure. This article will briefly describe the mechanics of an asset sale and equity sale, and then discuss some important items that are implicated depending on the chosen structure.

Equity Sales

A sale of equity involves the buyer, which may be an individual, group of individuals, or a company, purchasing the stock (in the case of a corporation) or interests (in the case of an LLC or partnership) of the business directly from the owner(s) of the equity. After the sale of the equity is consummated, the buyer takes the entire business as a whole, including all of the business’s assets and liabilities.

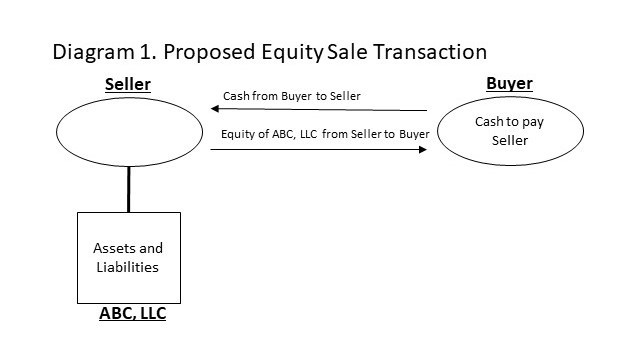

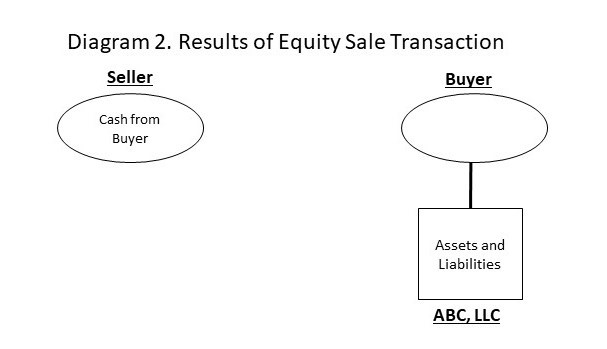

Diagram 1 shows the structure of a proposed equity sale. Note that ABC, LLC is the target company and owned by the seller prior to the sale. The buyer is proposing to transfer cash to the seller in order to purchase the equity of ABC, LLC. Diagram 2 shows the results of the transaction after the closing, with the buyer owning the equity of ABC, LLC and the seller now holding the cash from the buyer. Note that the buyer takes ABC, LLC with all of the assets and liabilities of the company and, except as may be agreed between the buyer and seller, the company is still responsible for satisfying all of the liabilities it had when it was owned by the seller.

{kind=link}

{kind=link}

Asset Sales

In contrast to an equity sale, a sale of the assets of a business involves the buyer (almost always an entity) purchasing only certain assets and assuming only certain liabilities of the target company. After the sale is consummated, the target company retains any unpurchased assets and liabilities that were not assumed by the buyer.

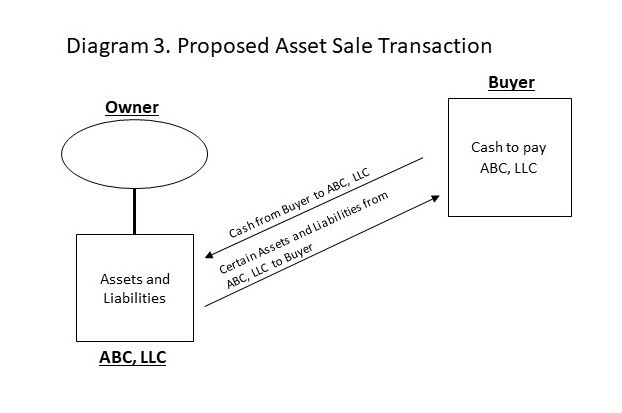

Diagram 3 shows the structure of a proposed asset sale. Note that ABC, LLC is the target company and the buyer is proposing to transfer cash to the target company in order to purchase certain assets and assume certain liabilities of ABC, LLC. Diagram 4 shows the results of the transaction after the closing, with the buyer owning the purchased assets and liabilities and the target company now holding the cash from the buyer, as well as certain retained assets and liabilities. This is an important distinction from an equity sale since the cash generated from the asset sale may now need to be used to pay off certain retained liabilities.

{kind=link}

{kind=link}

Impact of Structure

Tax Consequences

In an asset sale of a business with significant depreciable assets, the buyer will often receive a tax benefit while the seller may experience a tax disadvantage. This is because the purchase price in such an asset sale is often greater than the basis of the depreciable assets. This allows the buyer to receive a stepped-up basis in such assets and further depreciate the assets to reduce the buyer’s income. Meanwhile, the seller will have to pay taxes at the ordinary income rate for the difference between the assets’ basis and the purchase price.

In an asset sale without significant depreciable assets, the tax benefit to the buyer (and disadvantage to the seller) will generally be much lower.

In an equity sale, the seller typically receives a tax advantage because in most equity sales, the equity that is sold receives tax treatment as a capital gain (which is taxed at a lower tax rate than ordinary income). State rates for capital gains vary by state. In Nebraska, capital gains may be avoided altogether through the use of certain tax planning strategies.

There are also certain tax elections that may apply to some transactions that can provide benefits to both the buyer and seller. For example, a 338(h)(10) election made in connection with the sale of stock allows a seller to receive capital gains tax rates on the sale and the buyer to receive a stepped-up basis in the assets.

Treatment of Liabilities

As touched on above, in a sale of equity, all of the liabilities of the target company stay with the target company after the sale. This means that the seller of equity generally does not have to worry about responsibility for further liabilities of the company after the sale (although the seller will likely have agreed to backstop the buyer for certain undisclosed liabilities that may arise for some period after the closing).

Contrast this with an asset sale, where the buyer of the assets generally takes few liabilities. This means that the seller of the assets will remain responsible for future liabilities of the target company, and owners of the target company may thereafter remain liable for several years after dissolution. This is why asset sales are generally preferred by buyers and equity sales are generally preferred by sellers.

Assignment of Intangible Assets

In a sale of equity, contracts (such as leases, customer agreements, etc.) transfer with the target company by operation of law. This means that, unless any contracts have restrictions on a change of control of the target company, there is no need to obtain the consent of contract counterparties in order to consummate the transaction.

However, in a sale of assets, such transfer does not occur automatically, and most contracts will have a restriction on assignment without the consent of the counterparty. This can take considerable effort depending on the number of consents that are needed, and may jeopardize the confidentiality of the transaction. Thus, all other items being equal, a sale of equity is generally preferential if the target company has a large number of material contracts.

The bottom line is that the choice of transaction structure can have a significant impact on the pre-closing duties and post-closing obligations of the parties and have a direct effect on the amount of cash that the seller ultimately receives from the transaction. Thus, any business owner should seek competent legal advice to understand the risks and benefits of various transaction structures very early on in a potential sale process.